Sur le même sujet

-

FAQ sur la facturation électronique

- Facturation électronique

-

DORA - Campagne registre RoI 2027 - AMF

- Cybersécurité

-

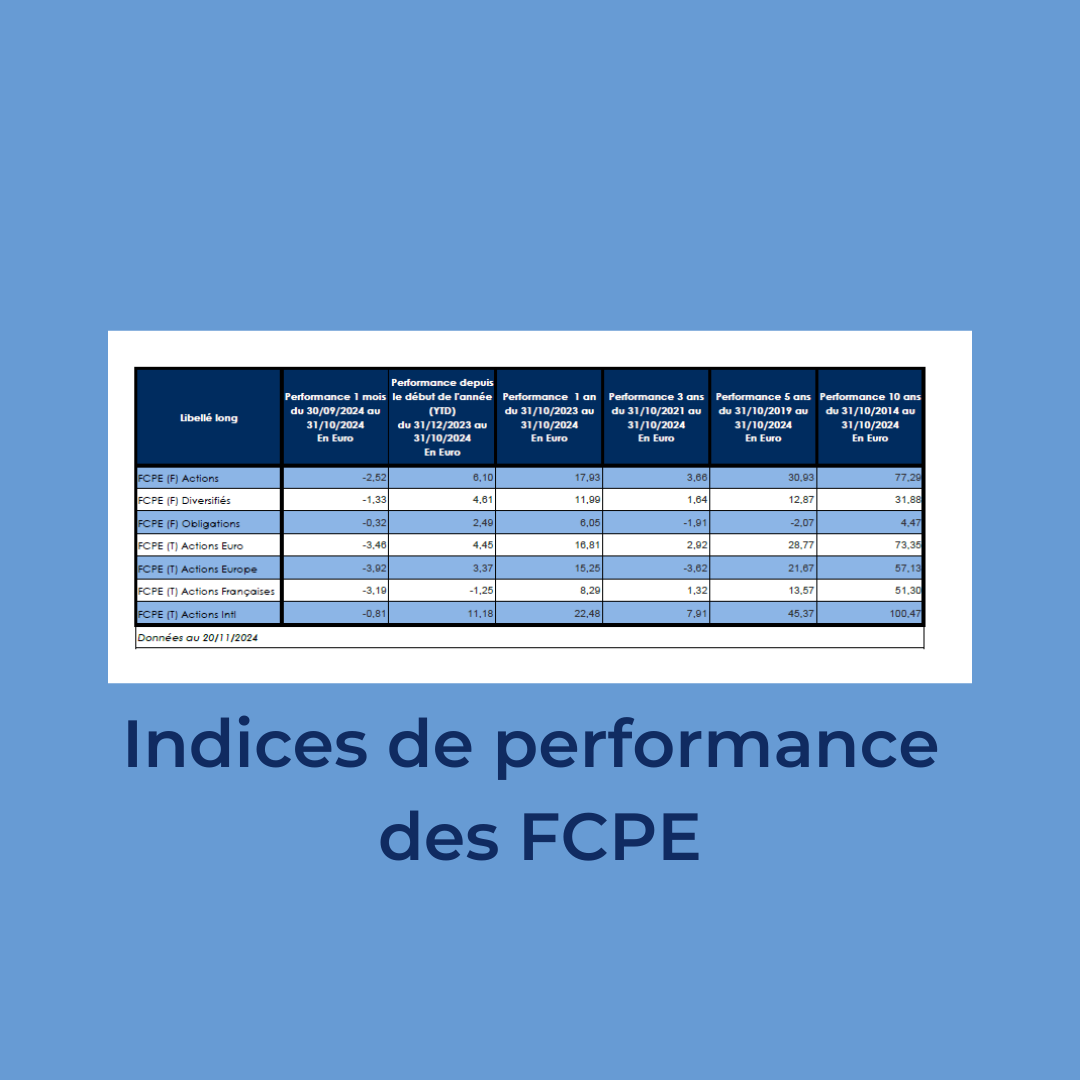

Indices de performance des FCPE du 31/12/1999 au 30/06/2026

- Epargne salariale